Imagine you’ve just finalized a breakthrough contract with a specialist in London or a tech vendor in Tokyo. You’re ready to hit “send” on that first payment, but then you pause, wondering if you’ve correctly handled the withholding tax singapore requirements. It’s a moment of hesitation we see often, where the excitement of global growth meets the anxiety of potential IRAS penalties. You want to focus on scaling your business, not worrying whether you’ve miscalculated a royalty rate or missed a filing deadline by a single day.

We understand that tax residency rules and cross-border payments can feel like a maze of technicalities. That’s why we’ve created this essential 2026 guide to give you back your confidence. You’ll learn exactly how to identify non-resident payees, apply the correct rates for everything from management fees to interest, and meet the 15th-day filing deadline every single time. We’re breaking down the complexities into a repeatable, automated process so you can treat compliance as a simple workflow rather than a source of stress. Let’s look at how you can protect your cash flow while staying perfectly aligned with the latest standards.

Key Takeaways

- Identify exactly when a vendor counts as a non-resident by applying the 183-day rule and company management criteria.

- Apply the correct rates for interest, royalties, and service fees to ensure your payments stay compliant with 2026 standards.

- Master the withholding tax singapore filing cycle to meet the 15th-day deadline and avoid unnecessary IRAS penalties.

- Discover how cloud accounting tools can automate your tax provisions and flag non-resident payments before you hit send.

- Follow a clear, step-by-step process for filing through the myTax Portal to eliminate manual errors and save time.

What is Withholding Tax in Singapore and Why Does It Matter?

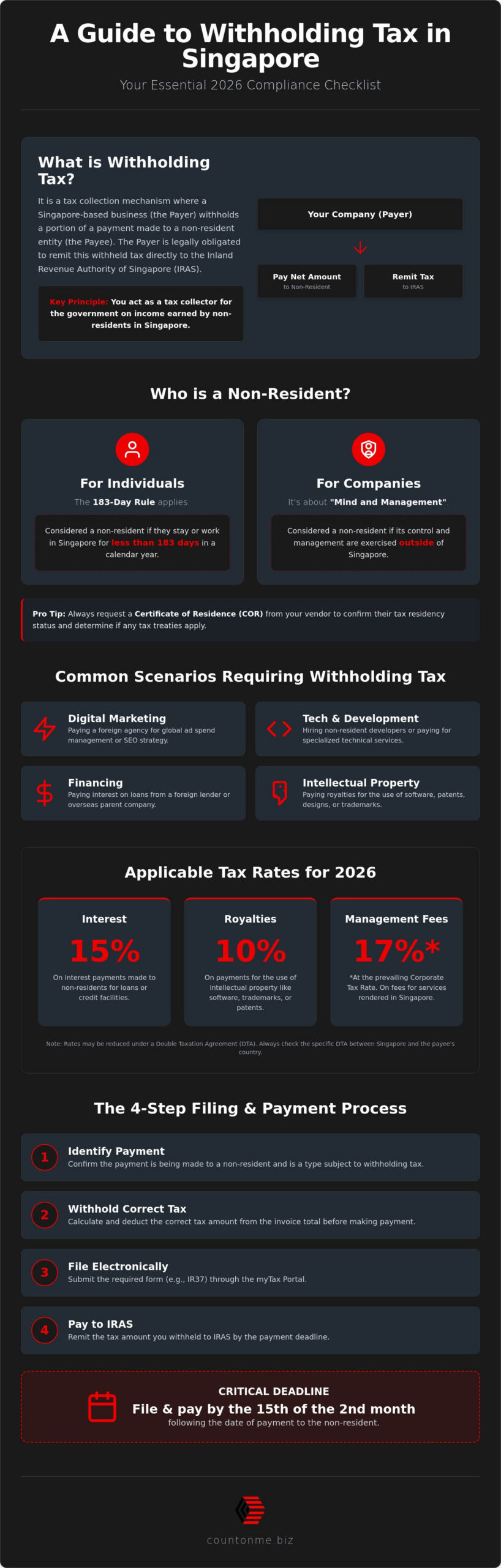

At its heart, withholding tax singapore is a mechanism where you, as the local business owner, act as a temporary tax collector for the government. It’s a system designed to ensure the Inland Revenue Authority of Singapore (IRAS) collects taxes from non-residents who earn income within our borders. Instead of expecting a foreign entity to file a tax return from thousands of miles away, the law requires the Singapore-based payer to deduct a portion of the payment at the source. If you’re looking for a broader perspective, What is Withholding Tax describes how this practice is used globally to prevent tax leakage in cross-border transactions.

In this dynamic, you are the “Payer” and your overseas partner is the “Payee”. IRAS places the burden of collection on you because you’re the one with the direct link to the local economy. It’s a fundamental part of the SME tax compliance in Singapore framework that every founder needs to grasp. When you pay a non-resident, you aren’t just settling an invoice; you’re fulfilling a statutory duty that protects the integrity of our tax system. We know this feels like extra homework, but understanding this relationship early prevents costly disputes with vendors later.

The Legal Obligation of the Singapore Payer

Your primary duty is to withhold the correct percentage of tax before the money ever leaves your account. This isn’t optional. If you pay the full invoice amount without deducting the tax, your company becomes personally liable to pay that missing tax to IRAS. Essentially, you’d be paying the vendor’s tax out of your own profits. Per 2026 IRAS guidelines, the point of payment is defined as the date the payment is due under the contract, the date the amount is credited to the payee, or the date the payment is actually made, whichever is earliest.

Common Scenarios for Singapore Startups and SMEs

Many founders encounter WHT requirements during their first year of scaling. We’ve seen these rules apply most frequently in these daily business operations:

- Digital Marketing: Paying a foreign agency to manage your global ad spend or SEO strategy.

- Tech Infrastructure: Hiring a non-resident software developer or paying for specialized technical services rendered in Singapore.

- Financing: Paying interest on a business loan sourced from a foreign lender or parent company.

- Intellectual Property: Distributing royalties for the use of proprietary software, designs, or trademarks within your Singapore operations.

By identifying these scenarios early, you can build WHT provisions into your contracts. This ensures your international partners understand why they’re receiving a net amount, keeping your business relationships as healthy as your compliance record.

Determining Tax Residency: Who is a Non-Resident?

One of the most common myths we encounter is the belief that simply incorporating a company in Singapore automatically makes it a tax resident. In reality, residency is less about where the paperwork is filed and more about where the “mind and management” of the business actually lives. If you’re paying a vendor and aren’t sure if they qualify as a resident, you should start by reviewing the official IRAS list of taxable payments to see if your transaction triggers an obligation. Understanding this distinction is the first step in mastering withholding tax singapore and protecting your business from compliance gaps.

To be certain about a vendor’s status, you should always request a Certificate of Residence (COR). This is a document issued by the tax authority of the vendor’s home country, proving they are tax residents there. If they can’t provide this, or if their presence in Singapore is temporary, you likely need to withhold tax. If you’re unsure how to evaluate a vendor’s tax status during onboarding, our team can help you build these checks into your workflow through our tax compliance and advice services.

The 183-Day Rule for Individuals

For individuals like foreign consultants or trainers, residency is often a numbers game. An individual is considered a non-resident if they stay or work in Singapore for less than 183 days in a calendar year. This math applies strictly to “contracts for service”, where you hire a freelancer or professional for a specific project. For example, if you hire a digital nomad to help with a 4-month software implementation project, they will likely fall under the 120-day mark. Because this is less than 183 days, they are a non-resident, and you must withhold tax from their final invoice. It’s a simple calculation, but missing it by just a few days can lead to errors.

Control and Management for Companies

For businesses, the test shifts from physical presence to strategic control. A company is a non-resident if its control and management are exercised outside Singapore. IRAS typically looks at where the Board of Directors meets to make high-level decisions. In 2026, remote board meetings are standard, but the location of the directors during those virtual sessions still matters. If your foreign-owned Singapore subsidiary has a board that makes all strategic choices from an overseas headquarters, it might be classified as a non-resident. This is a common trap for startups that are registered here but managed entirely by a founding team based in another country.

Payment Types and Applicable Withholding Tax Rates

Once you’ve identified that your vendor is a non-resident, the next step is determining how much to set aside. The rates aren’t one-size-fits-all; they depend entirely on the nature of the payment. For most SMEs, interest payments to non-residents attract a 15% rate, while royalties for using intellectual property are generally taxed at 10%. If you’re paying for management or technical services performed in Singapore, the withholding tax singapore rate usually aligns with the prevailing corporate tax rate of 17%. Keeping track of these varying percentages is much easier when you use A Founder’s Guide to Corporate Tax Filing in Singapore 2026 to plan your annual tax roadmap.

There are a few special cases to watch for. Payments to non-resident directors are subject to a higher rate of 24%, reflecting the personal income tax bracket for non-residents. Technical service fees can be tricky because they only apply if the service is rendered in Singapore. If your consultant performs the work entirely from their home office in another country, you might not need to withhold anything at all. We always suggest double-checking the location of service delivery before you finalize your payment calculations.

The Impact of Double Taxation Agreements (DTAs)

Singapore’s network of over 90 DTAs is a powerful tool for reducing your tax burden. These agreements with countries like the UK, Australia, and Vietnam often lower the standard rates significantly. In some cases, a 10% royalty rate might drop to 5% or even 0%. To benefit from these treaties, you must obtain a Certificate of Residence from your vendor and file Form IR586 with IRAS. It’s a small administrative step that can save your business thousands in cross-border transaction costs.

Calculating the Gross-Up: When You Absorb the Tax

We often see contracts where a vendor demands a “net” payment, meaning they want their full invoice amount without any deductions. If you agree to this, you’ll have to “gross up” the payment. This means you calculate the tax based on a higher total value so that the amount left after withholding matches the vendor’s original price. Essentially, your company is paying the vendor’s tax for them. Use the gross-up formula whenever your contract guarantees the payee a fixed amount regardless of local tax obligations.

Filing Procedures, Deadlines, and Avoiding Penalties

Once you’ve calculated the correct amount, the next step is getting that data to IRAS. The clock starts ticking the moment you make a payment to your non-resident vendor. In 2026, the deadline for withholding tax singapore remains the 15th day of the second month following the date of payment. For instance, if you pay an overseas consultant on July 20th, your filing and payment must be completed by September 15th. We recommend setting a recurring calendar alert for the 10th of every month just to give yourself a comfortable buffer. Managing your withholding tax singapore obligations isn’t just about avoiding fines; it’s about building a reputation for reliability with the tax authorities.

Filing is done through the IRAS myTax Portal. You’ll need to log in using your Singpass and navigate to the “Withholding Tax” section. The system will ask for the payee’s details, the nature of the payment, and the specific date the payment was made. Once submitted, you can choose from several modern payment methods. PayNow QR is often the fastest for one-off payments, but many of our clients prefer GIRO for its automated reliability. If you’re feeling overwhelmed by these monthly deadlines, our Tax Compliance & Advice team can manage the entire cycle for you.

Late Filing and Non-Payment Penalties

Missing a deadline is a common fear, and for good reason. IRAS applies a 5% penalty immediately if the tax isn’t paid by the due date. If the payment remains outstanding, an additional 1% penalty is added every month, which can eventually cap at 12% of the unpaid amount. We’ve found that IRAS is generally open to appeals if you have a valid reason, such as a technical glitch in the portal or an administrative oversight during a first-time filing. However, simply “forgetting” the date usually isn’t enough to get a penalty waived.

Amending a Withholding Tax Filing

Errors happen, even with the best intentions. If you realize you’ve under-withheld or used the wrong tax treaty rate, it’s best to act quickly. You can amend your filing through the myTax Portal by submitting a “Request for Amendment” form. We always encourage voluntary disclosure. If you spot and report an error before IRAS discovers it, you’re much more likely to avoid heavy fines or enforcement actions. Once an overpayment is confirmed, IRAS typically processes refunds within 30 days, though this can vary depending on the complexity of the case. By being proactive, you turn a potential crisis into a simple administrative correction.

Streamlining Withholding Tax with Cloud Accounting

Managing withholding tax singapore manually on a spreadsheet is a recipe for missed deadlines and calculation errors. In a fast paced business environment, you need systems that work as hard as you do. By leveraging modern cloud accounting services in Singapore, you can transform a complex legal requirement into a simple, automated workflow. Platforms like Xero and QuickBooks allow us to set up automated triggers that flag payments to non-resident vendors the moment an invoice is entered. This proactive approach ensures you never forget to withhold the necessary tax, protecting your cash flow from unexpected IRAS penalties.

The real magic happens when your accounting software provides real time visibility into your tax liabilities. Instead of waiting until the end of the quarter to realize you owe a significant sum, you can see your tax provisions update with every transaction. We believe that clarity is the best antidote to the stress of business management. When we act as your collaborative partner, we don’t just hand over a report; we provide a clear window into your financial health, ensuring you’re always prepared for the 15th day of the second month.

Automating the WHT Workflow

Setting up your digital infrastructure correctly is the first step toward compliance. We help you create specific tracking categories for foreign vendors so that every cross border payment is automatically categorized. By integrating your bank feed directly with tax provision accounts, the software can calculate the exact amount to withhold based on the rates we discussed earlier. You can even set up automated reminders that ping your phone or inbox well before the filing deadline, giving you total peace of mind.

The Value of On-Demand CFO Advisory

While automation handles the heavy lifting, some situations require a human touch and strategic insight. If you’re dealing with complex treaty questions or high value international contracts, consulting an on-demand CFO in Singapore can save you from expensive mistakes. We can help you structure your cross border agreements for maximum tax efficiency, ensuring you benefit from every available DTA relief. Our goal is to handle the technicalities of withholding tax singapore so you can focus on scaling your vision. Let’s work together to make your compliance process as modern and adaptable as your business itself.

Take the Stress Out of Global Growth

Expanding your reach beyond our borders is an exciting milestone, and managing cross-border payments shouldn’t be the thing that holds you back. By mastering the withholding tax singapore cycle, from identifying non-resident status to automating your provisions through cloud software, you’re doing more than just staying compliant. You’re building a scalable foundation that protects your cash flow and your reputation with IRAS. Remember that residency is about “mind and management” and that the 15th-day deadline is your most important recurring date for maintaining a clean record.

You don’t have to navigate these technicalities alone. As Xero-certified cloud accounting partners with over 20 years of experience in the Singapore financial sector, we specialize in making these complex workflows feel simple. We offer tailored packages for startups and SMEs, providing the steady support you need to scale with confidence. Simplify your tax compliance with Count On Me’s expert advisory and get back to what you do best: leading your business. We’re ready to act as your collaborative partner, ensuring your journey toward global growth is both stable and successful.

Frequently Asked Questions

Do I need to withhold tax if I pay a non-resident for services performed outside Singapore?

No, you generally don’t need to withhold tax if the service is performed entirely outside Singapore. Withholding tax singapore rules typically apply only when the non-resident professional or company provides the service while physically present in the country. However, we always recommend reviewing your specific contract to ensure the nature of the payment doesn’t fall under royalties or interest, which have different rules regardless of where the work happens.

What is the withholding tax rate for software-as-a-service (SaaS) payments?

Payments for standard SaaS subscriptions are usually exempt from withholding tax as they’re considered payments for a service rather than a royalty. If the payment involves the right to use a copyright or a deep level of technical customization, it might be classified differently under your contract. It’s best to classify these early in your cloud accounting system to avoid any confusion during your monthly filing cycle.

Can I file withholding tax annually instead of monthly?

No, withholding tax must be filed and paid on a per-transaction basis by the 15th day of the second month following the payment date. Singapore doesn’t offer an annual filing option for WHT because the system’s designed to collect tax at the source as transactions occur. Staying on top of this monthly requirement is much easier when you use automated reminders and provision accounts in your accounting software.

What happens if I forget to withhold tax and have already paid the vendor in full?

If you’ve already paid the vendor in full, your company’s still legally responsible for paying the tax to IRAS. You’ll need to pay the amount out of your own pocket and then attempt to recover it from the vendor, which can be a difficult conversation after the money’s gone. This is exactly why we emphasize checking a vendor’s residency status before you ever hit send on that first invoice payment.

Is withholding tax applicable to dividends paid to non-resident shareholders?

Dividends paid by Singapore-resident companies are not subject to withholding tax under our one-tier corporate tax system. This is a significant benefit for foreign shareholders and one of the reasons Singapore remains a top destination for global investment. You can distribute these profits to your non-resident shareholders without needing to deduct any tax at the source, keeping your capital structures simple.

How do I check if a country has a Double Taxation Agreement (DTA) with Singapore?

You can find the full list of over 90 Double Taxation Agreements on the IRAS website. These treaties are essential for reducing your withholding tax singapore rates, sometimes bringing them down to 0% for specific types of income. If you’re planning a major cross-border partnership, checking the specific treaty with that country should be your first step in your strategic financial planning.

What documents should I keep as proof of withholding tax payment?

You should maintain a digital file containing the confirmation of payment from the myTax Portal, the original vendor invoice, and the bank transfer record. Crucially, if you’ve applied a reduced treaty rate, you must keep a copy of the vendor’s Certificate of Residence (COR). These documents are your primary defense if IRAS ever conducts a routine audit of your cross-border transactions or filing history.

Can a non-resident professional claim back the tax withheld?

Yes, a non-resident professional can sometimes claim a refund if they choose to be taxed on their net income rather than the gross amount. They would need to file an individual income tax return in Singapore to declare their business expenses and offset the tax already withheld. It’s a more complex process, but it ensures they aren’t unfairly taxed on the costs they incurred while performing the work.